Beyond the Whale’s Reach: Lessons from the Sparrow on the Rupee’s Strategic Resilience

The reflections in “Beyond the Whale’s Reach: Lessons from the Sparrow on the Rupee’s Strategic Resilience” continue the civilisational and geopolitical thread opened in “Minnows and Marauding Whales: When History Returns to This Theme”. Read the opening article here.

If the earlier essay explored how smaller powers have historically confronted imperial overreach and predatory domination, this sequel turns inward to examine how resilience itself is cultivated — not merely through military or economic might, but through strategic patience, moral conviction, and collective endurance.

Drawing from another evocative episode in the Mahabharata, the new piece shifts the metaphor from whales and minnows to the humble sparrow confronting the sea, using that image to reflect on India’s evolving economic sovereignty and the rupee’s search for strategic space in a turbulent global order.

In the Udyoga Parva of Mahabharata, there is a story about a sparrow lamenting on the seashore when its eggs have been washed away by the sea. Garuda spots this bird moving to and fro along the shore, bringing a mouthful of water and emptying it on the shore. When quizzed by Garuda, the sparrow quipped that it was emptying the ocean waters as the Sagara king had not returned her eggs. The affronted bird king took this case to the Sagara king, and the eggs were retrieved. When facing a vast, liquid power, a minnow does not win through a head-on collision of scale, but through the relentless accumulation of structural credibility that eventually compels the whales of the global market to adjust.

In the earlier essay, the question was whether smaller powers can withstand the pressure of larger ones. History suggested that they can do so, but only when protected by some form of shield: moral authority, narrative endurance, institutional depth, or strategic timing. Economics offers no such romance.

“Let Pharaoh proceed to appoint overseers over the land and take one-fifth of the produce of the land of Egypt during the seven plentiful years. And let them gather all the food of these good years that are coming and store up grain.” (Genesis 41:34–35)

“Joseph gathered grain in great abundance, like the sand of the sea, until he ceased to measure it, for it could not be measured.” (Genesis 41:49)

Joseph’s wisdom in Egypt lay not in predicting famine alone, but in constructing a shield before scarcity arrived. Granaries became instruments of sovereignty. When neighbouring kingdoms weakened, Egypt endured because it had converted years of plenty into strategic reserves.

Kautilya explicitly says a king without a full treasury cannot wage war, conduct diplomacy, or sustain administration. “Koshomulam Rajyam” — the treasury (kosha) is the root of the kingdom. Modern states behave similarly. Foreign exchange reserves, energy buffers, and fiscal discipline are today’s granaries against geopolitical famine.

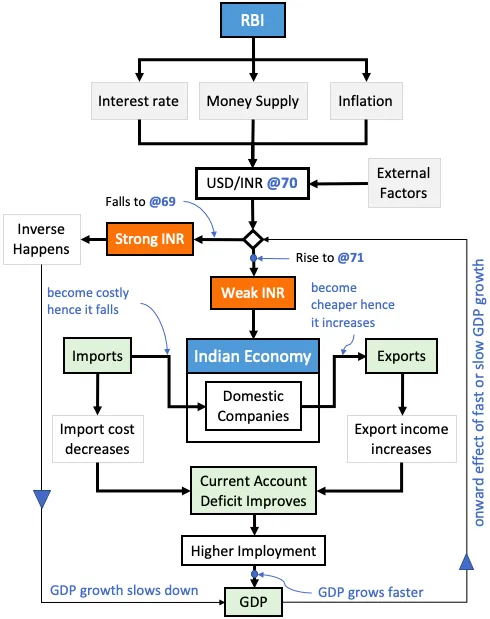

Today, power rarely arrives only through armies or declarations. It arrives through currencies, bond yields, payment systems, sovereign ratings, capital flows, sanctions architecture, and technology denial. The whale no longer needs to breach the shoreline. It can move exchange rates, alter liquidity, tighten sanctions architecture, or redirect capital with a few signals from financial markets.

The minnow, therefore, requires a different kind of shield.

The most successful example of such shielding in modern times is China. For nearly three decades, China resisted the natural appreciation of its currency despite enormous export competitiveness. By accumulating vast foreign exchange reserves and maintaining strict control over capital flows, Beijing effectively prevented the renminbi from floating freely against the U.S. dollar. This was not merely monetary policy. It was geopolitical statecraft disguised as exchange-rate management.

China’s advantage, however, rested on foundations that India does not possess in equal measure. China enjoyed persistent trade surpluses, manufacturing dominance, and deep integration into global supply chains. Dollars flowed into China faster than they flowed out. India operates differently. It runs structural trade deficits, imports energy heavily, and relies more on services exports and capital inflows than merchandise surpluses. This difference matters enormously.

A country with a trade surplus can defend its currency with accumulated reserves. A country with a trade deficit often defends its currency with confidence alone. And confidence is among the most volatile assets in economics.

Yet minnows are not without options. Economic history is filled with states that survived not through brute financial strength, but through intelligent asymmetry.

When Ben Bernanke merely hinted at tapering Quantitative Easing in 2013, the rupee fell from around 54 to nearly 69 against the dollar within months. Raghuram Rajan stepped in as RBI Governor and stabilised the currency through a combination of NRI bond issuance, rate signalling, and communication credibility — not just reserves.

The Swiss National Bank unilaterally abandoned its euro peg in 2015, causing a 30% currency spike in minutes. Even disciplined, reserve-rich minnows can be overwhelmed when they resist market forces too long, and the costs of sudden reversal are catastrophic. Sequencing matters as much as shielding.

Brazilian Finance Minister Guido Mantega explicitly used a tax on hot capital inflows (2009–2013) to dampen currency appreciation, calling it part of a “currency war.” It worked, until it did not. When the commodity cycle turned and foreign capital retreated rather than surged, the controls were quietly dismantled, exposing the fact that Brazil had used the interval to defend the real but not to restructure the economy that the real represented. Unorthodox tools can create space; only structural reform can fill it.

Consider Singapore. It lacks the territorial scale or military heft of larger powers, yet its currency remains remarkably stable because the state built credibility brick by brick: disciplined fiscal policy, strong reserves, export sophistication, and institutional predictability. The Singapore dollar is protected not by emotional nationalism, but by the quiet accumulation of trust.

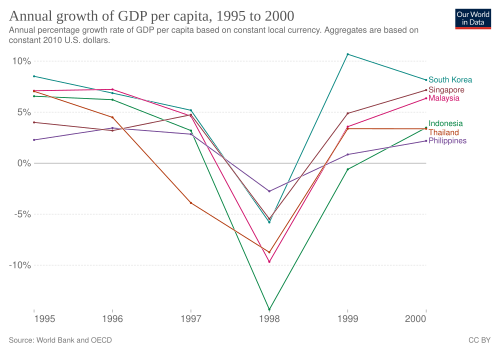

Or take South Korea after the 1997 Asian Financial Crisis. The country realised that dependence on volatile external borrowing could become an existential vulnerability. Seoul responded by building massive forex reserves, encouraging domestic industrial champions, and reducing short-term external fragility. The lesson was stark: sovereignty in the modern world depends as much on balance-sheet resilience as on military preparedness.

Even Malaysia under Mahathir Mohamad offered a controversial but revealing example during the Asian crisis. When speculative attacks battered the ringgit, Malaysia imposed capital controls rather than fully submit to market orthodoxy. At the time, many Western economists condemned the move. Yet Malaysia stabilised faster than several peers. The episode demonstrated that smaller economies occasionally survive by rejecting textbook purity in favour of pragmatic sequencing.

This tension between markets and sovereignty has long divided economists.

Milton Friedman argued that freely floating exchange rates act as natural shock absorbers. In his view, markets distribute pressure more efficiently than states can. Yet the world that emerged after globalisation complicated that optimism. Capital moves faster than democratic institutions. Currency markets often punish perception long before fundamentals deteriorate.

Joseph Stiglitz repeatedly warned that unfettered capital mobility can destabilise developing economies, especially when financial liberalisation outpaces institutional maturity. For Stiglitz, the problem was not markets themselves, but the asymmetry of power within global markets. Some countries write the rules; others merely absorb them.

Albert O. Hirschman argued that developing economies rarely advance through symmetrical growth. Progress, in his framework, comes through deliberate imbalances — by creating forward and backward linkages that pull investment, capability, and institutional adaptation in their wake. The strategist’s task is not to build everything at once, but to identify those pressure points where a concentrated investment compels the wider system to reorganise around it.

For India, the currency question is inseparable from this logic. A rupee defended by reserves alone is a rupee dependent on the kindness of capital flows. A rupee defended by structural indispensability is something more durable. India’s Unified Payments Interface (UPI) already processes more real-time digital transactions than any other country on earth — a quiet but significant Hirschmanian linkage, already compelling global fintech architecture to orient towards Indian standards.

India’s generic pharmaceutical industry supplies roughly forty percent of the United States prescription drug demand; during the pandemic, this leverage became visible. India’s engineering services exports underpin infrastructure, aerospace, and technology projects across three continents.

These are not ornamental achievements to cite in diplomatic communiqués. They are the structural foundations of monetary credibility. When a country becomes load-bearing within the global economy — when its disruption would cost others more than they can easily absorb — the whale begins to swim more carefully around the shore. Hirschman called this the logic of linkage. In the context of the rupee, it is the logic of earned sovereignty: not borrowed, not inherited, but built, sector by sector, until the asymmetry itself becomes the shield.

Dani Rodrik, in his “Trilemma” (or the “Impossible Trinity”), argues that countries cannot simultaneously maintain a fixed exchange rate, free capital movement, and independent monetary policy — they must sacrifice one. India has implicitly chosen to sacrifice exchange-rate stability in favour of retaining monetary policy autonomy and managing (not freely floating) capital.

Barry Eichengreen’s work on the “exorbitant privilege” of the dollar argues that the dollar’s reserve status gives the United States the unique ability to borrow in its own currency and export inflation. India’s Vostro settlement experiment is, in part, a small attempt to chip away at this dollar privilege in bilateral contexts.

These theoretical debates — between market efficiency and sovereign protection, between free capital and managed stability — are not merely academic. They are the architecture within which every rupee defence decision is made. Friedman’s world assumes symmetric information and neutral capital. Stiglitz’s world recognises that the rules are written by those who benefit from them. Hirschman’s world goes further: it suggests that the structurally weaker party need not simply absorb these rules, but can, over time, rewrite its position within them by cultivating indispensability. India’s task is to move from being a price-taker in global capital markets to being, in at least some strategic domains, a terms-setter. That is not a fantasy. It is a project, and it requires a different kind of policy imagination than either pure liberalisation or reflexive protectionism can offer.

What then are India’s shields?

Not a single weapon, but layers of insulation.

First, deeper domestic manufacturing. Every imported semiconductor, solar module, or defence component is also imported vulnerability. The Performance Linked Incentive Scheme points in the right direction, but only if implementation remains disciplined: with sunset clauses enforced, performance thresholds genuinely tested, and rent-seeking by incumbents resisted. A subsidy that rewards presence rather than performance merely shifts dependence from foreign suppliers to domestic ones without building the underlying capability.

Second, energy diversification. No currency weakens faster than one financing expensive energy dependence during geopolitical turbulence.

Third, gradual internationalisation of the rupee in bilateral trade settlements. This is not an immediate replacement for dollar dominance, but it reduces marginal exposure.

Fourth, stronger sovereign balance sheets. Countries with fiscal credibility survive storms longer because markets believe they can absorb pain.

Fifth, patient reserve accumulation. Foreign exchange reserves are not merely accounting entries; they are strategic deterrents.

Finally, institutional predictability. Investors tolerate nationalism more easily than unpredictability. Markets fear volatility more than ideology.

This is where the metaphor of shields returns.

Some shields are visible, like armies and alliances. Others are invisible, like reserve buffers, fiscal discipline, export ecosystems, trusted institutions, and credible central banks. Modern minnows survive not because whales disappear, but because they learn how not to be swallowed whole.

The temptation for every rising nation is to mistake symbolism for insulation. Temples may inspire confidence. Political rhetoric may rally domestic audiences. Civilisational memory may strengthen resolve. But currencies are defended by productivity, reserves, credibility, and institutional trust.

In the ancient world, Kashi’s shield lay in the aura of Shiva. In the modern world, the shield is less mystical and far more unforgiving. It lies in balance sheets, trade structures, capital controls, industrial policy, and the confidence that a nation can endure pressure longer than markets expect.

The whale has evolved. The minnow must evolve faster. If the first lesson was how to survive the whale, the second is how to make the whale respect the shore the minnow is building.

A deeply layered and thought-provoking piece by Ramesh Krishna that goes far beyond currency debates and explores the larger question of India’s economic sovereignty. Beyond the Whale’s Reach intelligently uses the metaphor of the sparrow and the whale to explain how resilience, adaptability, and strategic patience can matter more than sheer financial might. The article offers a sharp perspective on the rupee’s evolving role in a shifting global order, while reminding readers that true economic strength lies in stability, confidence, and long-term vision. An insightful and timely analysis.